Geopolitical Insights of Ukraine Russia Conflict on Supply Chains (Part 2)

The list of companies defined by the Yale School of Management has grown from 400 to more than 1,200 counting. Almost 1,000 companies have publicly announced they are voluntarily curtailing operations in Russia beyond the bare minimum legally required by international sanctions, but some companies have continued to operate in Russia undeterred.

See below for a summary of company positions as of today:

-

WITHDRAWAL (Grade A) - 334 companies

-

SUSPENSION Grade B) - 455 companies

-

SCALING BACK (Grade C) - 152 companies

-

BUYING TIME (Grade D) - 160 companies

-

DIGGING IN (Grade E) - 244 companies

A full list can be accessed by following this link: Almost 1,000 Companies Have Curtailed Operations in Russia—But Some Remain | Yale School of Management

Perhaps some of the more notable/well known Remainers (Group F) are: Alibaba, Ariston Group, Aveya, Braun, Calzedonia, Check point software (counter cyber security), Etam, Giorgio Armani, Koch Industries, Makita, Mitsubishi, OBO Bettermann, Raiffeisen Bank International, Syngenta, Vaillant Group, so or all of which will undoubtedly struggle to comply with new legislation fully now and in the future.

Original classification form Yale School of Management:

- WITHDRAWAL - Clean Break: companies completely halting Russian engagements/exiting Russia;

- SUSPENSION - Keeping Options Open for Return: companies temporarily curtailing operations while keeping return options open;

- SCALING BACK - Reducing Activities: companies scaling back some business operations while continuing others;

- BUYING TIME - Holding Off New Investments/Developments: companies postponing future planned investment/development/marketing while continuing substantive business;

- DIGGING IN - Defying Demands for Exit: companies defying demands for exit/reduction of activities

The response has not been universal and different organizations will have different or competing motives for their actions. For procurement and supply leaders’, alignment with your organization’s strategy will continue be key in this area. However, this may test certain employee positions as the company strategy and personal codes may not be fully aligned. Time will of course be a key arbiter in this space.

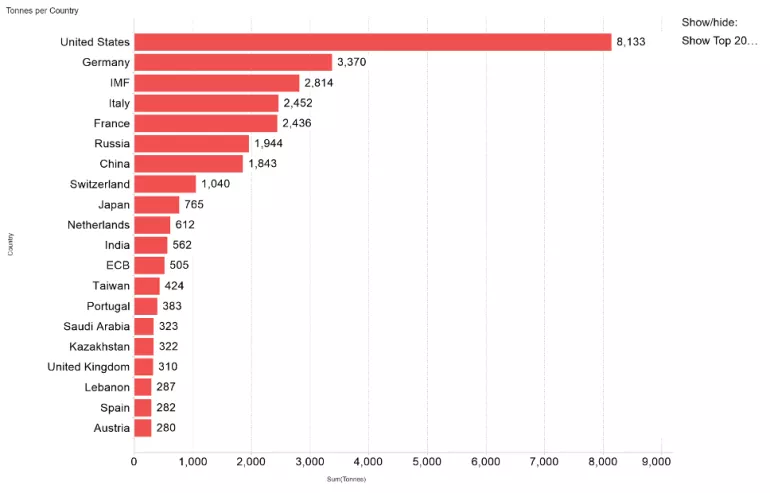

Monetary sanctions and counter measures continue to be debated with a variety of views and commentary being offered. The outcome of this means that for each entity they must carry out due diligence salient to them and their supply chains in order to be able to make effective decisions both now and in the future. Some points to consider will be that since the end of WWII, the US dollar has been used as the world’s reserve currency, accounting for about half of all global trades, loans and debt, helping to anchor the international monetary system. Other stable currencies such as the Swiss Franc. British pound and more recently the Australian dollar have also been used in the same way. However, this war in particular could spell the end of the US dollar and other stable currencies use and see the emergence of gold as a new common fiscal anchor. As can be seen from the table below there is a wide contract in the top 20 countries:

Source: www.suissegold.eu

Russia’s invasion in Ukraine has caused precious metals prices to jump as supply remains low, consistent supply is uncertain and therefore demand continues to grow stronger. Specifically, Russia supplies 15% of the world’s platinum, has a 40% share of the world’s palladium, (which makes it the world’s largest producer), and is the second largest gold producer. Further, the sanctions imposed on Russia along with its removal from the SWIFT Banking system will also provide large obstacles to export its precious metals, consequently increasing their value as demand grows.

The automobile industry is increasing its production in 2022 as the global semiconductor supply chain crisis eases. This production is driving demand for precious metals like platinum, palladium, and rhodium. These industrial metals are key components of autocatalytic converts; technology used to lower emissions. Rhodium alone has recorded a 67.52% increase in its value since the start of 2022. Palladium has increased 34.60% this year and is expected to continue if supply decreases and demand increases.

Conversely though Lithium, another natural earth rare metal is produced outside of the Ukraine & Russia currently. However, there is rapidly increasing demand and therefore supply will be an issue. For context in 2020, lithium production was slightly above 0.41 million metric tons of LCE; in 2021, production exceeded 0.54 million metric tons (a 32% Y-on-Y increase). Sources suggest that lithium demand of 3.3 million metric tons or a compounded 25% growth rate. Interestingly, most of the current sources of lithium comes from Australia, Latin America, and China (accounting for a combined 98% on a 2020 baseline). An announced pipeline of projects will likely introduce new players and geographies to the lithium-mining map, including Western and Eastern Europe, Russia, and other members of the Commonwealth of Independent States (CIS). This reported capacity base should be enough for supply to grow at a 20 percent annual rate to reach over 2.7 million metric tons of LCE by 2030.

Another key metal to look towards is palladium with Russia being the largest producer, it is evident that these sanctions will heavily affect palladium’s value. While exports might drop due to the sanctions, the supply shortage is expected to boost prices.

As reported before there are other areas that are critical to global supply chains such as wheat, fertilizers, sunflower oil, corn, etc all of which will undoubtedly support the analysis and commentary in relation to food supply chain shortages in the months to come. A recent illustration by McKinsey (May 2022) illustrated it a shown below:

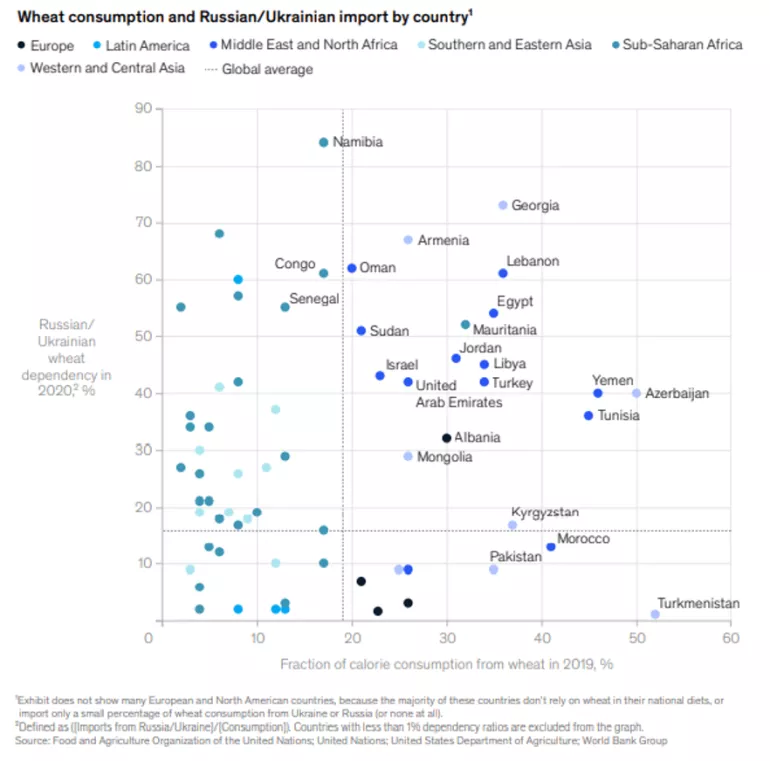

This is exacerbated by other factors such as the Indian government declaring that it will not allow exports of wheat and other substantive food products, only those that are supported by pre-existing foreign exchange notes prior to the declared export ban. However, the primary countries to eb impacted by the primary food crops will be the Middle East, North Africa, Western and Central Asia, as illustrated in the chart below, also by McKinsey (May 2022).

Looking across the food commodities in particular, whist there have been some minor changes and easing the overall picture shows growing and future increases, supporting the issues raised regarding a food supply issue to come.

Source: https://tradingeconomics.com/commodity

Turning to the essential aspect of energy we can see that there are many issues from currency, supply links to high dependency countries from Russia, such as Germany and Hungary, etc. However, in the wake of this the pursuit of ESG strategies and in particular the net-zero commitments will be put under strain as a consequence. In particular three factors as impediments to key instruments such as the interruption of supply of key materials, products and services from the Ukraine, economic sanctions against Russia, and reduced economic cooperation between nations. In the context of energy, a report by Pippa Stevens stated, “since the war began a substantial influx of capital into renewable energy funds has taken place, reversing a multi-month downward trend”. A clear signal that companies are taking alternative approaches and so it could be argued the war has acted as catalyst for good. However, complexity, challenges and indeed the very access to rare earth metals will all have a bearing on this.

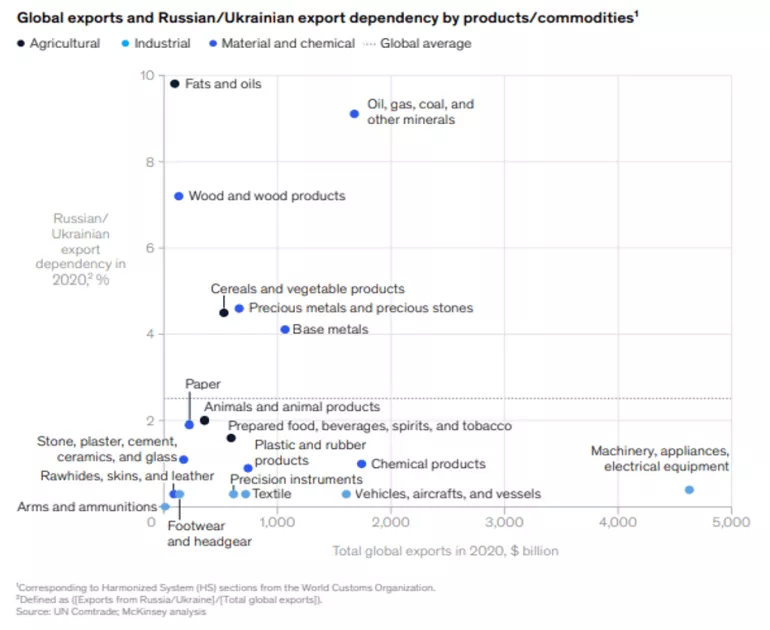

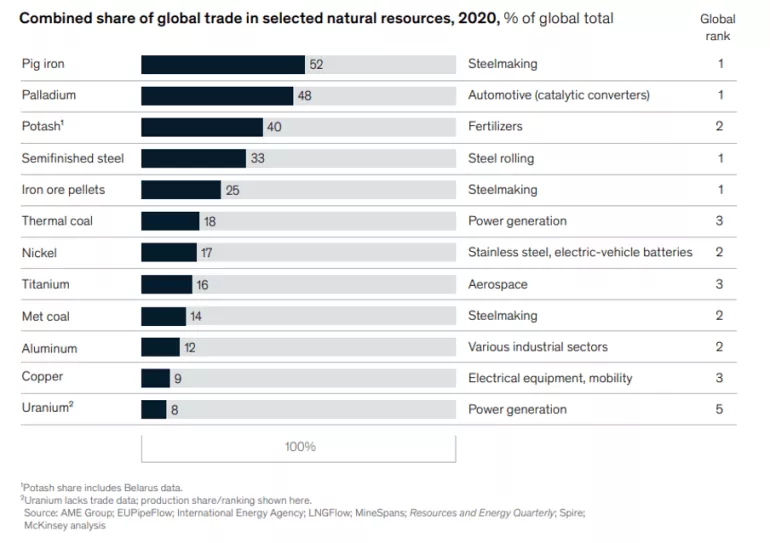

There are a number of positive investments into the start-up community, which are being supported by groups such as the NetZero Technology Centre ( Net Zero Technology Centre (netzerotc.com) anchored in Aberdeen, Scotland, who I have had the pleasure of collaborating with. However, a key topic of debate is and will continue to be, amongst many others, the supply chains they will be able to construct and lean into to drive availability of the products that feed into the likes of wind turbines, energy saving technology, solar and alternative energy generation, etc. Therefore, we should note the Ukraine and Russia both have a significant share of global trade in many commodities, as mapped by McKinsey:

In terms of impacted sectors, we can again see that whilst manufacturing is an obvious candidate those also under pressure will be:

- Aerospace & Defense

- Automotive

- Consumer products (white goods, durables, etc.)

- Energy producers (both current and alternative)

- Construction & Property

- Technology

- Logistics and freighting

- Farming/agriculture (seeds, fertilizers, and machinery)

This current and ongoing fragility will undermine economic recovery in many and diverse direct and indirect ways and is unlikely to be short term.

According to the Aljazeera news bulletin (25th May 2022) Time is running out to export some 24 million tonnes of grain stuck in grain silos, out of Ukraine before the country’s new harvest as Russian forces continue to blockade the country’s Black Sea ports. Further, there is now no room to store the country’s next grain harvest in existing viable grain silos or those that have been damaged in the war. According to Ukrainian lawmaker Yevheniia Kravchuk at the Davos summit last week the Ukraine has about a month and a half before farmers start to collect the new harvest.

The issue from a logistics point of view is the ports of Odesa, Chornomorske and others cut off from the world by Russian warships and the grain supply can only travel on Ukraine’s congested land routes that are far less efficient and/or safe. During the discussions at Davos, but independent of them via The Interfax news agency earlier cited Russian Deputy Foreign Minister Andrei Rudenko as saying Moscow is ready to provide a humanitarian corridor for vessels carrying food to leave Ukraine, in return for the lifting of some sanctions. European Commission Chief Ursula von der Leyen on Tuesday (24th May 2022) called for talks with Moscow on unlocking wheat exports trapped in Ukraine by the sea blockade.

Additional Read: Geopolitical Insights of Ukraine Russia Conflict on Supply Chains (Part1)

Resources

Stevens, P., Lithium’s vital role in the energy transition sends prices to record highs. How to play it. 15/05/22

Crispeels, P., Robertson, P., Somers, K., and Wiebes, K., Outsprinting the energy crisis. May 2022

Olivia White, Kevin Buehler, Sven Smit, Ezra Greenberg, Mihir Mysore, Ritesh Jain, Martin Hirt, Arvind Govindarajan, and Eric Chewning. War in Ukraine: Twelve disruptions changing the world. May 2022

Russian and Ukraine commodities review: base metals (https://country.eiu.com/Ukraine/ArticleList/Analysis/

Simchi-Levi, D., and Haren, P., How the war in the Ukraine is further disrupting global supply chains, March 2022

John E. Katsos, Jason Miklian, and John J. Forrer. In Light of Russia Sanctions, Consider Your Conditions for Doing Business in Other Countries. 15th March 2022

Yale School of Management: Almost 1,000 Companies Have Curtailed Operations in Russia—But Some Remain | Yale School of Management

Gold reserves by country: www.suissegold.eu

Commodity prices: https://tradingeconomics.com/commodity

Recommended blogs

Popular blogs

June 11, 2025 4 min read

The Suite Approach: 4 reasons why an integrated S2C solution is a game changer

Read more

June 9, 2025 2 min read

Which eAuction type is right for you? A guide to smarter auctions with Scanmarket by Unit4

Read more

August 8, 2025 4 min read

What is eProcurement? A Complete Guide to Electronic Procurement

Read more

June 17, 2025 2 min read

Enabling Sustainable Supplier Management with Scanmarket by Unit4

Read more

June 3, 2025 5 min read

The hidden cost of your contracts: Unlocking savings with Contract Management

Read more

January 22, 2025 4 min read

Procurement’s Role in Driving the Triple Bottom Line through ESG and Technology

Read more